The Unseen Hand: Unravelling the Financial Complicity That Reshaped Scottish Football

Pulling back the curtain on how financial complicity between David Murray and Gavin Masterson impacted Scottish football for decades.

13 years after the death of Rangers Football Club 1872, and with the re-emergence of David Murray - the catalyst behind the collapse of the club - and his claims that Celtic supremo Peter Lawwell had far too much influence in Scottish Football, I take a look at the financial dealings involving the former Rangers owner and the Bank of Scotland’s former managing director Gavin Masterson - over a pattern of preferential lending, corporate pressure, and starkly contrasting treatment towards rival clubs.

The alliance between the duo not only sustained Rangers’ ambitions through escalating debt but also sought to undermine Celtic Football Club’s financial stability and played a direct role in the downfall of Airdrie Football Club.

The 1990s: A Period of Financial Transformation

The 1990s marked a significant period of financial evolution for Scottish football. Clubs across the UK faced immense pressure to modernize their infrastructure, largely driven by the stringent safety requirements of the Taylor Report, which mandated the conversion of stadia to all-seater venues following the Hillsborough disaster.

The report necessitated substantial capital investment, placing considerable financial strain on many clubs - including Celtic.

Celtic found itself in a troubling position, burdened by £9 million in debt and facing the formidable expense of complying with the Taylor Report. This financial demand meant that clubs were not merely sporting entities but businesses under immense financial pressure, making them highly susceptible to external funding and the influence of their banking relationships.

This era also intensified the historic rivalry between Rangers and Celtic, extending beyond the pitch into corporate and financial spheres. The significant financial demands imposed by the Taylor Report created an environment where clubs were highly vulnerable to debt and reliant on external funding, amplifying the impact of any alleged preferential banking relationships or targeted financial pressures.

The "Special Relationship": Murray, Masterton, and Rangers' Escalating Debt

The financial relationship between David Murray's business empire, which included Rangers Football Club, and the Bank of Scotland, particularly during Gavin Masterton's tenure, was extraordinary. David Murray was widely recognised as the golden boy of Scotland during the Thatcher years, a prominent businessman whose diversified Murray Group encompassed interests in steel, mining, property development, and venture capital. Rangers Football Club was however the flagship investment of this empire, confirming its central role in Murray's public profile and overarching financial strategy.

At the core of the complicity was the relationship between David Murray and Gavin Masterton, who served as the Bank of Scotland's managing director. This connection is a key factor influencing the bank's lending decisions - digging deep to back Murray, and willingly increasing his business empire’s overdraft facility, further suggesting an unusually accommodating approach to his borrowing requirements. An internal report from Lloyds, which later acquired Bank of Scotland, further backed this up, revealing that "money was thrown at Sir David Murray’s company because he was dynamic, astute and successful," and was considered "one of Bank of Scotland’s favoured sons". Strongly supporting the notion of preferential treatment.

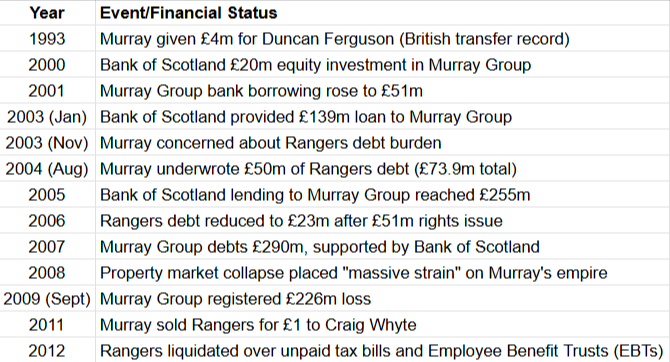

The scale of borrowing was substantial and escalated significantly over time. The Murray Group's bank borrowing rose from £51 million in 2001 to £139 million in 2003, £255 million by 2005, and reached £290 million by 2007, all explicitly supported by Bank of Scotland.

Examples of this support, include £4 million provided to Murray in the summer of 1993 for the signing of Duncan Ferguson - a British transfer record fee at the time. Demonstrating the bank's willingness to fund significant football investments.

When Rangers was demerged from Murray Group into a separate holding company and received a £60 million loan, due upon its sale, and Murray himself underwrote £50 million of the football club's debt, which reached £73.9 million in 2004. These immense financial commitments from both Murray and the bank were instrumental in sustaining Rangers' operations and ambitions.

The consistent and extensive nature of the Bank of Scotland's lending to the Murray Group and Rangers, particularly as debt levels mounted, points towards a preferential financial relationship that transcended beyond typical commercial risk assessments. This alleged collusion, rooted in the personal connection between Murray and Masterton, allowed Rangers to engage in what has been described as financial doping, enabling the club to maintain a competitive edge through spending that might have been unsustainable under conventional financial scrutiny.

The bank's continued support, and its ownership of 11.5% of the company by 2007, suggests a deeply intertwined financial arrangement. This extensive backing, by enabling spending beyond what might have been possible under stricter financial conditions, distorted the competitive balance in Scottish football, suggesting that financial power, rather than purely sporting merit, played a significant role in the Rangers’ success during this period.

The following table provides an overview of key financial milestones for the Murray Group and Rangers, illustrating the significant and escalating involvement of the Bank of Scotland:

Key Financial Milestones of the Murray Group and Rangers (1993-2012)

The Demise of Airdrie: Debt Enforcement and Corporate Influence

David Murray's direct involvement in the financial collapse of Airdrie Football Club presents a stark contrast to the financial leniency extended to Rangers. There is clear evidence that through his non-footballing company, Carnegie, Murray applied for an interdict for a relatively modest £30,000 debt owed by Airdrie FC. This action led to Rangers, under Murray's chairmanship, directly "arrest[ing] the club's share of the gate receipts" from a Scottish Cup tie. Significantly impacting Airdrie's immediate cash flow, adding to their already precarious financial state.

Murray's justification for this aggressive action was presented as a pragmatic business decision: "I feel very sorry for Airdrie and their supporters but we're running a business". However, the consequences for Airdrie were severe. The evidence explicitly states that Rangers FC, through the actions of their then Chairman Sir David Murray, was a "key participant in forcing Airdrie FC into administration" and ultimately into liquidation. Furthermore, Murray and Rangers were "responsible for the deaths of TWO clubs: Airdrie FC and Clydebank FC, suggesting a pattern of leveraging financial power to eliminate other clubs.

There is no evidence to directly implicate Gavin Masterton or the Bank of Scotland in Airdrie's specific demise due to the £30,000 debt, but the Airdrie case serves as a powerful illustration of David Murray's willingness to use his corporate power and the influence of Rangers to aggressively enforce debts, even against smaller clubs, leading directly to their demise. This action stands in sharp contrast to the immense and escalating debt Rangers accumulated under Murray's ownership, which was consistently supported by Bank of Scotland.

Demonstrating a highly selective and opportunistic application of financial rigor. Murray, whose own empire was sustained by hundreds of millions in bank debt, was ruthless in enforcing a comparatively tiny debt against a struggling club, leading to its destruction. This suggests a strategic use of financial power not just for recovery, but potentially to eliminate perceived obstacles and to assert dominance without regard for the smaller entity's survival. This incident underscores the significant power in Scottish football that he had and the predatory actions his business practices, where the financial vulnerability of smaller clubs could be exploited. It also serves as a crucial precedent for understanding the attempts to bring down Celtic, indicating a wider strategy of financial dominance and control within Scottish football.

The Battle for Celtic: Bank of Scotland's Attempts to Block Fergus McCann's Takeover

The allegations surrounding the Bank of Scotland's actions during Fergus McCann's takeover of Celtic Football Club form a central pillar of the complicity. In the early 1990s, Celtic faced a dire financial situation, burdened by £9 million in debt and the substantial costs associated with complying with the Taylor Report. The incumbent Kelly-White regime was widely viewed as having exhausted its resources and support, prompting thousands of fans to rally behind a campaign to end the families dynasty. This created an urgent and critical need for new investment and a change in ownership to secure the club's future.

Fergus McCann, who ultimately saved Celtic, directly accused Gavin Masterton, representing the Bank of Scotland, of attempting to "thwart his Celtic takeover in March 1994". This involved a deal orchestrated between Masterton and David Smith, a Celtic board member described as "friendly with the Bank". Proposing a deal aimed to facilitate a takeover by Gerald Weisfeld, a significant customer of the Bank of Scotland. Crucially, McCann asserted that this arrangement was designed to "take the bank off the hook" for Celtic's existing debt and provide "cash for the families" (the outgoing board members), but would provide "no new investment in Celtic". This further suggests a self-serving arrangement that prioritised the bank's and the outgoing board's financial interests over the long-term health and necessary regeneration of the football club.

The Bank of Scotland exerted significant pressure on the Celtic board, demanding personal guarantees. Critically, the bank set a "deadline for foreclosure to seize the assets" of Celtic. This aggressive tactic was employed despite McCann having already deposited £11 million to demonstrate his capital and willingness to invest in the club. Following his successful takeover, one of McCann's first actions was to move Celtic's account away from the Bank of Scotland. He explicitly stated that this was to remove the club from the "control of Masterton and co. who were busy propping up Murray’s debt mountain at Ibrox". This statement directly links the bank's actions against Celtic with its ongoing, extensive financial support for Rangers.

The stark contrast in the Bank of Scotland's approach to Celtic versus Rangers forms a key component of the complicity between Masterson and Murray. While the bank aggressively pursued foreclosure and attempted to install a preferred buyer for Celtic, it was simultaneously described as "busy propping up Murray’s debt mountain at Ibrox".

This was a deliberate strategy of financial manoeuvring aimed at influencing the competitive balance of Scottish football. This goes significantly beyond standard banking practice and was a coordinated effort to disadvantage one club for the benefit of another, driven by institutional biases and allegiances within the Scottish establishment. This stark disparity in treatment was not accidental nor solely based on objective risk assessment. There was a clear strategic intent to influence the competitive landscape by weakening Celtic's ability to rebuild effectively (by attempting to block McCann's investment) while ensuring Rangers' continued financial strength under Murray.

The following table provides a direct comparison of the Bank of Scotland's financial interactions with Rangers and Celtic during this critical period:

The Unasked Questions of Scottish Football Journalism

A significant aspect of this historical narrative is the lack of critical scrutiny from Scottish journalism regarding David Murray's financial dealings and the alleged complicity with the Bank of Scotland’s Gavin Masterson. There is certainly a clear perception of a compliant press or even a lapdog loyal press in Scotland, particularly concerning coverage of Rangers and its then-powerful owner. There was a clear reluctance or inability within certain media outlets to critically challenge the dominant narratives surrounding the club and its financial operations.

The pertinent question of "why no journalist in Scotland has ever asked questions of Murray over this complicity" is frequently raised by fans of numerous clubs. Gutter press like the Daily Record and The Sun, have no interest in truth, knowledge or actual investigative journalism and instead prioritise telling their dwindling audience what they think they want to hear in the hope that they hit their readership targets.

A significant failure was the media's inability or unwillingness to adequately research Craig Whyte before Murray sold Rangers to him, despite the alarm being raised at the start of 2011 by fan bloggers. This further highlights a fundamental failure of journalistic due diligence. The criticism extends to the period of Rangers' collapse, as nobody bothered to ask the questions that needed to be asked in 2012.

David Murray's claims that Peter Lawwell tried to bury Rangers is laughable given the lengths Murray went to with collusion from Masterson. The media's role in failing to challenge this narrative is a continued point of contention.

The consistent failure of a significant portion of mainstream Scottish journalism to critically investigate the financial complicity surrounding David Murray and Rangers, suggests a deep-seated systemic bias or a fundamental lack of journalistic independence. This inaction not only allowed powerful figures to largely control their own narrative and evade accountability for actions like the Employee Benefit Trust (EBTs) scheme but also contributed to a distorted public understanding of events. This erosion of trust in media fuels a culture where financial doping and corporate manipulation could thrive unchecked with a lack of accountability within the Scottish establishment.

Legacy, Accountability, and Lingering Questions

The complex web of financial relationships and corporate manoeuvres that significantly impacted Scottish football during the late 20th and early 21st centuries, clearly points to a pattern of alleged complicity between David Murray and the Bank of Scotland, through Gavin Masterton, which manifested in several critical ways.

Firstly, the Bank of Scotland provided sustained and preferential financial backing to David Murray's business empire and Rangers Football Club. Characterised by extensive and escalating lending, allowing Rangers to operate with significant financial leverage aka financial doping. This level of support, even as Murray's businesses accumulated substantial debt, went beyond conventional banking prudence, enabling a period of considerable spending and sporting success for Rangers.

Secondly, a stark contrast emerged in the Bank of Scotland's approach to Celtic Football Club. While heavily supporting Rangers, the bank engaged in aggressive tactics to undermine Celtic's financial stability and thwart Fergus McCann's takeover. The attempts to facilitate a deal that would provide no new investment for Celtic, coupled with the threat of foreclosure despite McCann's demonstrated capital, suggest a coordinated effort to disadvantage one club for the benefit of its rival.

Thirdly, David Murray's direct and ruthless role in the financial demise of Airdrie Football Club, through the aggressive enforcement of a relatively small debt, further highlights a selective application of financial rigor. This action stands in sharp contrast to the leniency and extensive support his own club received, underscoring a potential strategic use of financial power to assert dominance within the Scottish football landscape.

The long-term consequences of Murray’s and the bank’s actions are profound. They contributed to the financial instability and eventual liquidation of Rangers, while Celtic, despite facing immense challenges, demonstrated resilience and achieved subsequent success under new leadership.

The significant role played by the Bank of Scotland, the Murray Group, and certain sections of the Scottish media shaped the narrative and financial outcomes within Scottish football. The biases and a lack of independent oversight allowed these dynamics to persist, leading to a culture where accountability was often elusive.

These events leave lingering questions about transparency and accountability within Scottish football's financial and corporate spheres. The failure of robust journalistic scrutiny further exacerbates these concerns, suggesting that a more vigilant and independent media would have helped to ensure accountability of Rangers Football Club, David Murray, Gavin Masterson, and the Bank of Scotland.

And that’s before we even contemplate bringing Dunfermline into the equation and the web that Murray sewed with the Fife club and the late Jimmy Calderwood - before Masterson led the club to the brink of liquidation just a year after Rangers died.